But when we talk about retirement with our clients, we also encounter a touchy subject: end of life.

Americans are beginning to retire later and later: the average retirement age is now 62 (the age that you can begin drawing on Social Security). However, Social Security benefits increase between the ages of 67 and 70, which means that many retired adults are choosing to wait to start their Social Security. Smart, right?

There’s just one thing: The average life expectancy in the U.S. ranges from 76-79 years, depending on which source you’ve found. This means that the average American only begins pulling from their Social Security about 10 years before average life expectancy ends.

As financial planners, it’s our duty to discuss this timeline with clients — and to find alternative financial solutions that can help them and their families prepare for the expected and unexpected.

Of course, navigating discussions about retirement, end of life, and death is tricky. Some clients are incredibly open to the need for this type of planning while others are not. It’s essential to learn how to guide your clients through this sensitive and complex process. Here, we’ll walk you through how to host end-of-life planning discussions while also empowering clients to prepare for the best — a very long, healthy life.

Starting the discussion about end-of-life planning

“So the question really becomes… How long are you planning on living?” This was a conversation that we recently asked inside of our Amplified Planning CORE monthly course — and it’s truly the underlying question when we talk to our clients about retirement.

None of us knows how long we will live, and discussing emotional events like retirement and the end of life in one session can quickly derail a financial planning meeting.

That’s why it’s important to:

- Get to know the client before diving into these conversations (understand their backgrounds, family life, beliefs, etc.)

- Build trust and connection in your first meeting (we show you how to do this inside Amplified Planning!)

- Ask about their preferences and wishes for retirement BEFORE talking about end-of-life

- Ask questions about the legacy they’d like to leave

- Ask about any experiences that left an impression regarding end of life, i.e. watching a loved one struggle with estate and probate after an unexpected death

- Use phrases other than “end of life” or “death”

- Leave plenty of time for questions and offer clients time to think about their wishes before they make decisions

No matter, what the goal is to assure clients that planning for retirement and old age is a proactive and positive step. It allows them to maintain control over their future and ensures their wishes are honored.

From there, you can guide the discussion to cover all elements of retirement and long-life planning.

Planning for life expectancy in retirement

No one can see the future. However, to plan for the future, we as financial planners have to take a few factors under advisement. For one, when calculating retirement needs, we have to have an estimated life expectancy for our clients. This estimation might take into account things like:

- Family history (especially illness or age of death for immediate family members)

- Medical history

- Environmental factors, like smoking, alcohol use, workplace safety, etc.

- Lifestyle (exercise, eating habits, family life, community connections, work, charity, etc.)

It’s up to you and your client to decide on an average life expectancy — and to be realistic about what’s financially required to support them comfortably through that age (and beyond).

Once you have a target life expectancy in mind, you can use that to create a financial plan that helps your clients live their preferred lifestyles in retirement and beyond. To do that, consider these factors:

Social Security early vs. delayed benefits

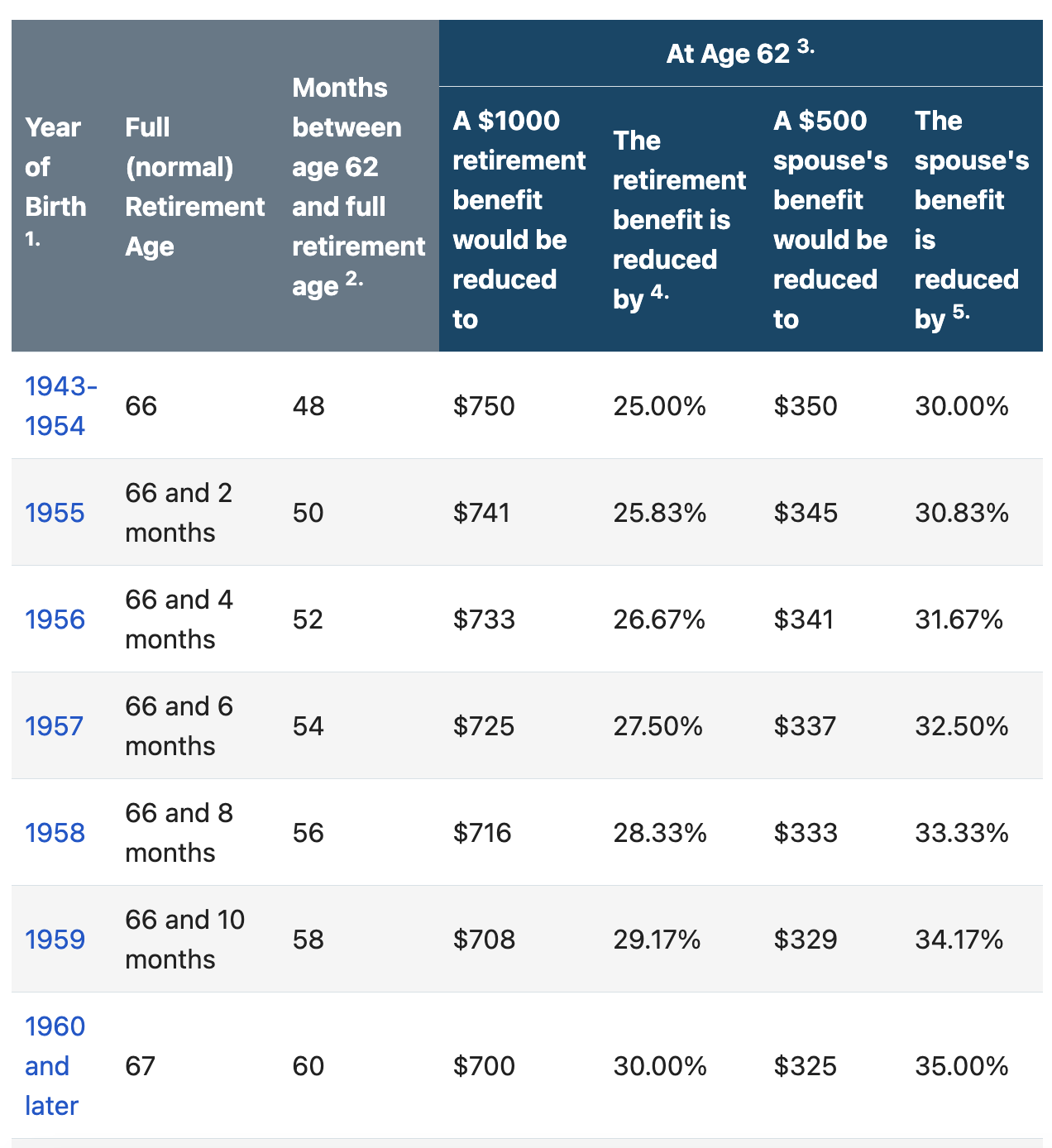

As mentioned above, the average age of retirement is currently 62. However, Social Security benefits hit their highest point at age 70 (see chart below). The break-even point for taking Social Security is 82. This means that, if a person lives past 82, the numbers tell us they should wait until age 70 to retire.

If your clients want to retire fully before age 70, it’s important to discuss alternative retirement funding options with them.

NOTE: Not all clients have Social Security benefits and not all of them believe that it will be there when they retire. This is where alternative retirement and long-life planning options become priority.

Marriage & partners’ life expectancy

Alongside an individual’s Social Security benefits, you should also consider your client’s spouse or partner’s life expectancy. Survivor benefits decrease the older the main beneficiary is, which is another motivating factor in early vs. delayed draws.

Image sourced from The Social Security Administration

Savings

Speak with your client about the need and purpose of having savings, such as an emergency fund, to help them prepare for life’s uncertainties. Having savings (not just retirement accounts) means that they are in a better position to continue to contribute towards their retirement as well as have a proper budget in place once they are in retirement.

As financial planners, we need to help clients understand the delineation between savings and retirement accounts. It helps to view savings as funds for short-term expenses, and retirement accounts as funds for future expenses.

Retirement accounts

Many clients will assume that, once they retire, they do not contribute to their retirement accounts anymore. This is where you can show them how continuously contributing to their tax-advantaged accounts, like employer-sponsored plans or IRAs, allows them to leverage compounding interest without the impact on taxes during the accumulation phase (while they are saving for retirement). Without the immediate impact of taxes on their fund, their money can grow faster and sustain them for a long life!

Spending

Discussing lifestyle and goals in retirement is important because a client who wants to travel or have a higher-cost lifestyle will have different spending needs than a client who plans to age at home with minimal additions to their lifestyle.

When you have an idea of the lifestyle your client wants, you can calculate a post-retirement budget by combining monthly spending, taking into account Social Security, retirement account withdrawals, and/or other income sources. You can also subtract expected spending and expenses (adjusting for at least 3% inflation) to determine the viability of their retirement plans — and adjust accordingly.

Tax rate of return

Failing to account for taxes could derail your plan and your client’s financial future. That’s why it’s so important to consider the tax rate of return. The tax rate of return refers to the anticipated annual return on investments after accounting for taxes. It’s an important metric, as it provides a more accurate depiction of the actual gains realized from their investments. This figure takes into consideration an individual’s tax bracket, which determines the portion of their investment returns that will be owed in taxes. By factoring in taxes, your clients can make more informed decisions about their investment strategies and accurately assess their overall financial performance.

Healthcare costs (especially long-term care)

Healthcare is often the most significant end-of-life expense. Your client’s financial plan should account for projected/potential medical costs, including insurance premiums, out-of-pocket expenses, and potential long-term care needs.

This is also a great time to discuss long-term care insurance and Medicare supplementation to ensure the protection of plans and accounts.

Housing & living expenses

Depending on your clients’ plans and lifestyle, you might want to discuss the costs associated with aging in place, assisted living, and/or nursing home care.

Funeral and burial expenses

Funeral and burial costs can be substantial. Include these expenses in your clients’ projections, whether that’s increased life insurance, savings, and/or pre-paid funeral plans.

Legal and administrative costs

End-of-life planning also involves legal and administrative representation (and expenses). Make sure to talk to your clients about healthcare proxies and power of attorney to ensure that they are covered if and when something happens. Helping them decide on end-of-life care and burial wishes is also important, as is budgeting for these expenses to limit the strain on their family or representatives.

Life happens: How to adapt plans as clients age

The most important thing to note about planning for a post-retirement life is that… life happens. Clients will change jobs and condense 401ks. They will move. Some will get sick or lose a spouse. Some will get divorced and decide on a new path for their retirement. This is part of the art of financial planning — adapting to your clients’ lives.

But every client will have a different approach to life and how they want to live into their old age. Some clients will have more of a “YOLO” approach to life and money, while others will be focused on saving enough to support themselves as they age (or leaving a legacy for their families).

To balance this out, it’s important to ask clients:

- What their short-term goals are (6 mos. – 5 years)

- What their long-term goals are (5+ years)

- What they want to accomplish personally before they retire

- What they want to accomplish personally after they retire

- If they want to leave a legacy (and how they define a legacy)

- If they envision themselves relocating or moving after retirement

- If they plan to work in retirement (in any capacity)

- If they plan on retiring at all!

At the end of the day, your goal is to understand your clients and create a plan that reflects their values.

You may encounter a client who doesn’t want to save for retirement – or save for a potentially long life. Your job will be to help them save for the unexpected, and to find ways to continue to drive income for as long as they do live. You may also encounter clients who don’t want to spend anything now for fear they’ll need it later. Helping these clients understand their numbers can empower them to enjoy life a bit more now, instead of waiting for retirement (or worse, never enjoying the fruits of their labor).

Retirement planning & end-of-life discussions in action

These conversations highlight how financial planning is so much more than projections on a spreadsheet — it’s a profession that helps people live better. It’s also our job, as financial planners, to turn hard conversations into empowering ones. We can turn talk of death and life expectancy into a powerful conversation about the legacy our clients want to live.

If you want to learn how to host conversations about retirement, end-of-life planning, and the changes life brings, join us inside Amplified Planning.

Amplified Planning offers monthly financial planning courses, during which you’ll meet clients and couples from different walks of life, with a variety of financial scenarios and needs. For example, two recent courses dive into the nuances of retirement planning and navigating emotional conversations around differences in partners’ views of retirement, end-of-life planning, low retirement savings, and more.

Meet Jeff & Jenny

They’re in their 50s… and realizing that retirement is fast-approaching. They haven’t prioritized retirement savings, though, and they need to catch up. This is, of course, tied up in conversations about death, because they’ve had several friends die recently who were also their age.

Meet Sarah & Steeve

These two are parents to teen children, and Steve thinks about death all the time. This changes the dynamics of the end-of-life conversations and how they want to support their children if something were to happen.

Of course, these are just two of the courses inside our massive financial planning learning library.

If you’d like to see how we approach these unique scenarios for retirement and long-life planning — and earn 50 CFP Board Standard Pathway hours for each completed course — join Amplified Planning. There, you can access a library of client courses that will help you learn advanced strategies for retirement planning, end-of-life discussions, Social Security optimization, and more.

Join us today and take your financial planning career to the next level!